Income Tax is one of the most significant pillars of India’s financial system. It is more than just a law—it is a social contract between citizens and the State. Through taxes, individuals and businesses contribute to the common pool, which the government then redistributes in the form of infrastructure, social welfare, healthcare, education, and national defence. In short, paying tax is not merely a legal duty—it is a civic responsibility.

In this article, we’ll dive deep into the fundamentals of Income Tax in India, its structure, recent developments, and its role in shaping the country’s economy.

1️⃣ What is Income Tax?

Income Tax is a direct tax levied by the Government of India on the income earned by individuals, Hindu Undivided Families (HUFs), firms, companies, LLPs, and associations of persons. Unlike indirect taxes (such as GST, which is collected at the point of sale), income tax is directly paid by the taxpayer to the government.

The law governing income tax in India is the Income-tax Act, 1961, which has undergone numerous amendments to keep pace with economic changes, policy shifts, and evolving global standards.

2️⃣ Who is Liable to Pay Income Tax?

The liability to pay income tax arises when a person’s income exceeds the basic exemption limit prescribed under the law. For the Assessment Year 2025-26, the exemption thresholds vary depending on the regime chosen:

- Under the old regime, with deductions and exemptions, the limit is generally ₹2.5 lakh for individuals below 60 years, ₹3 lakh for senior citizens (60–80 years), and ₹5 lakh for super senior citizens (80+ years).

- Under the new regime, which offers reduced tax rates but removes most exemptions, the basic exemption limit has been raised to ₹3 lakh for all individuals.

Apart from individuals, the following entities are also required to pay income tax if they earn taxable income:

- Hindu Undivided Families (HUFs)

- Partnership Firms & LLPs

- Domestic and Foreign Companies

- Associations of Persons (AOPs)

- Trusts

3️⃣ Heads of Income

The Act classifies income under five broad heads. Understanding them is crucial for accurate filing and tax planning:

- Income from Salary – Wages, pensions, allowances, perquisites, and bonuses.

- Income from House Property – Rent earned or deemed rent from property ownership.

- Profits and Gains of Business or Profession – Income earned from business operations or self-employment.

- Capital Gains – Profits from transfer of capital assets like property, stocks, or mutual funds.

- Income from Other Sources – Interest income, winnings from lotteries, dividends, etc.

Each head has its own set of deductions and computation methods.

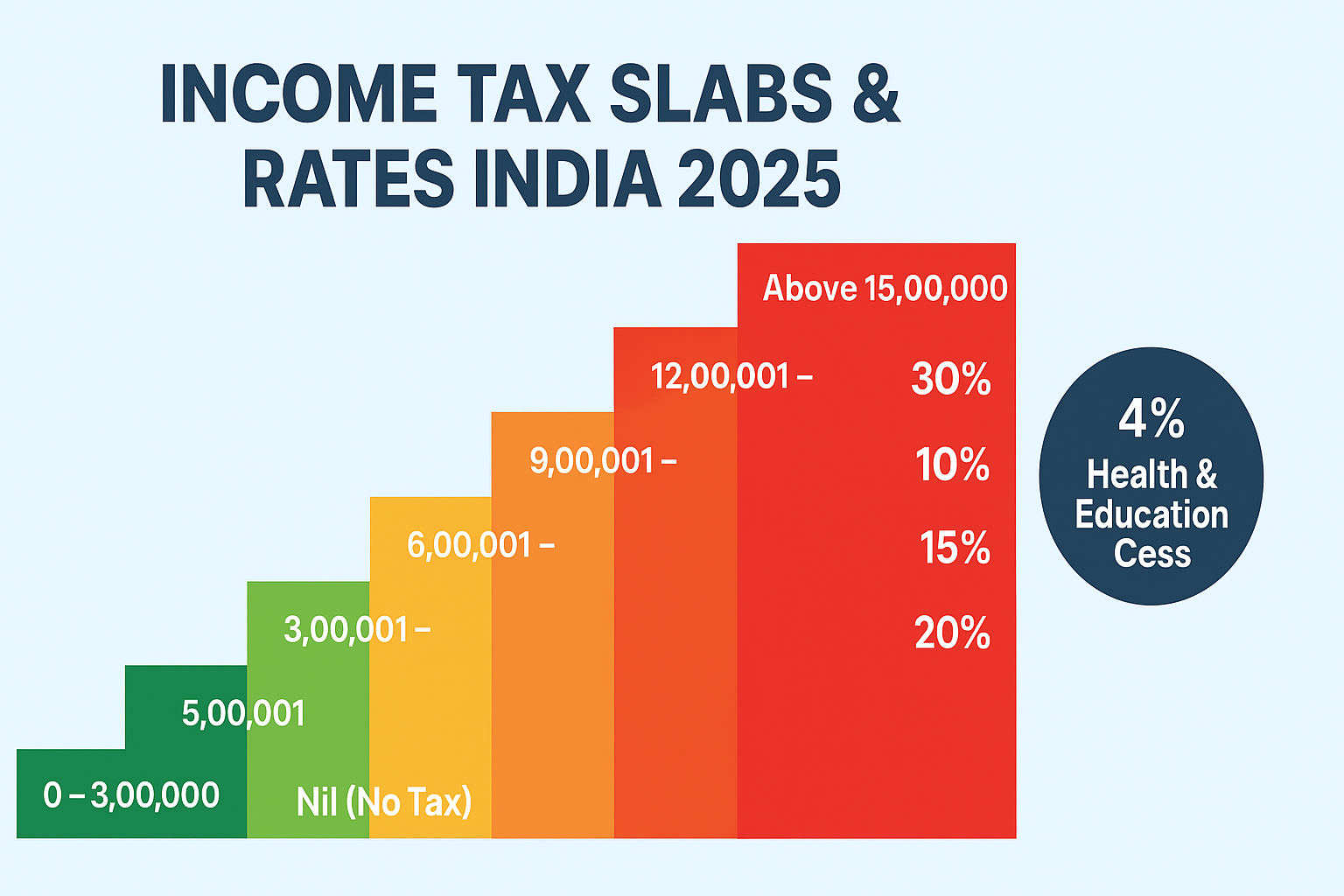

4️⃣ Tax Regimes in India

Since 2020, taxpayers in India have had the option to choose between two regimes:

Old Regime:

- Higher tax rates.

- Numerous exemptions and deductions available (HRA, 80C, 80D, 80G, home loan interest, etc.).

- Suitable for taxpayers with significant investments and expenses that qualify for deductions.

New Regime:

- Lower tax rates, simplified structure.

- Very limited deductions and exemptions allowed.

- Favours those who prefer straightforward taxation without complex planning.

For AY 2025-26, the new regime has been made the default option by the government, though taxpayers can still opt for the old regime while filing returns.

5️⃣ Filing of Income Tax Returns (ITR)

Every eligible taxpayer is required to file an Income Tax Return (ITR) annually. Filing not only helps in reporting income but also in claiming refunds, carrying forward losses, and establishing financial credibility.

Due Dates for AY 2025-26:

- 31st July 2025 – For individuals and HUFs not subject to audit.

- 31st October 2025 – For companies and audit cases.

Filing late may attract penalties under section 234F and interest under sections 234A/B/C.

6️⃣ Deductions and Exemptions

Deductions allow taxpayers to reduce taxable income, thereby lowering tax liability. Some popular ones (mainly under the old regime) include:

- Section 80C: Investments in PPF, ELSS, Life Insurance, EPF (limit ₹1.5 lakh).

- Section 80D: Health insurance premium.

- Section 80G: Donations to charitable institutions.

- Section 24(b): Interest on home loan (up to ₹2 lakh).

The new regime has eliminated most of these benefits, but a few remain (like employer’s NPS contribution).

7️⃣ Importance of Paying Income Tax

Many taxpayers view tax as a burden. However, income tax plays a critical role in nation-building:

- Infrastructure Development: Roads, highways, metros, airports.

- Healthcare & Education: Public hospitals, schools, scholarships.

- Social Security: Welfare schemes for the underprivileged.

- Defence & Security: Maintaining armed forces and internal security.

- Digital India: Expanding internet access, e-governance, and fintech.

In simple words, every rupee paid in tax fuels India’s growth story.

8️⃣ Penalties for Non-Compliance

Tax evasion or failure to comply with tax provisions invites strict consequences. Penalties may include:

- Late filing fees (₹1,000 to ₹5,000 under section 234F).

- Interest on unpaid tax.

- Prosecution in cases of deliberate concealment.

The Income-tax Department has become increasingly tech-driven, with data-matching, PAN-Aadhaar linkage, and information sharing between banks, GST, and other agencies, making evasion more difficult.

9️⃣ Recent Developments in Income Tax

The Indian taxation system is evolving rapidly. Key trends include:

- Faceless Assessments: Reducing human interaction, minimizing corruption, and ensuring transparency.

- Pre-filled ITRs: Simplifying return filing with pre-populated data from banks, employers, and stock exchanges.

- Technology Integration: AI-driven scrutiny, data analytics, and e-verification.

- Shift Towards New Regime: Government incentives to nudge taxpayers towards simplified taxation.

🔟 Conclusion

Income Tax in India is not merely a financial obligation—it is the backbone of democracy and development. By contributing honestly, taxpayers ensure that the country continues to progress, balancing economic growth with social justice.

Yes, taxes may feel burdensome at times, but imagine a nation without them—no roads, no public hospitals, no affordable education, no security. In that sense, tax is not money lost; it is money invested in the collective future.

As India grows into a $5 trillion economy and beyond, the tax system will continue to evolve—becoming more digital, more transparent, and hopefully, more equitable. The responsibility, however, lies with both the government (to utilize funds wisely) and the citizens (to comply sincerely).

⚖️ In the words of U.S. Supreme Court Justice Oliver Wendell Holmes:

“Taxes are what we pay for a civilized society.”

And nowhere does this ring truer than in today’s India.

Leave feedback about this